While many of our contractors are navigating the PPP loan program, we wanted to make sure we had some information available on the Forgiveness Application. For those who like to skim and find the most relevant information to their needs, we also wanted to put out our video transcript. If you have additional questions that we didn’t answer yet, get in contact with us! We’re here to support the construction industry with any financial questions.

Transcript:

Hey there! It’s Karine Woodman with 24hr Bookkeeper. Today I’m going to talk about the PPP loan forgiveness application. I am going to do a basic overview of completing the three worksheets that are part of the application, one of them being the application. Keep in mind that there are changes coming in the pipeline, such as instead of an 8-week PPP period that is proposed, to change from 16 to 24 weeks. Also the 75/25 payroll versus non-payroll costs are proposed to switch to a 60/40 split. For the sake of this video, I’m going to do it as it sits today, and keep in mind that that application could change. I’m guessing that the majority of the information is going to remain the same. It’s just again the extension of the time will be different, in addition to the split. But you’ll still have those costs.

Table of Contents

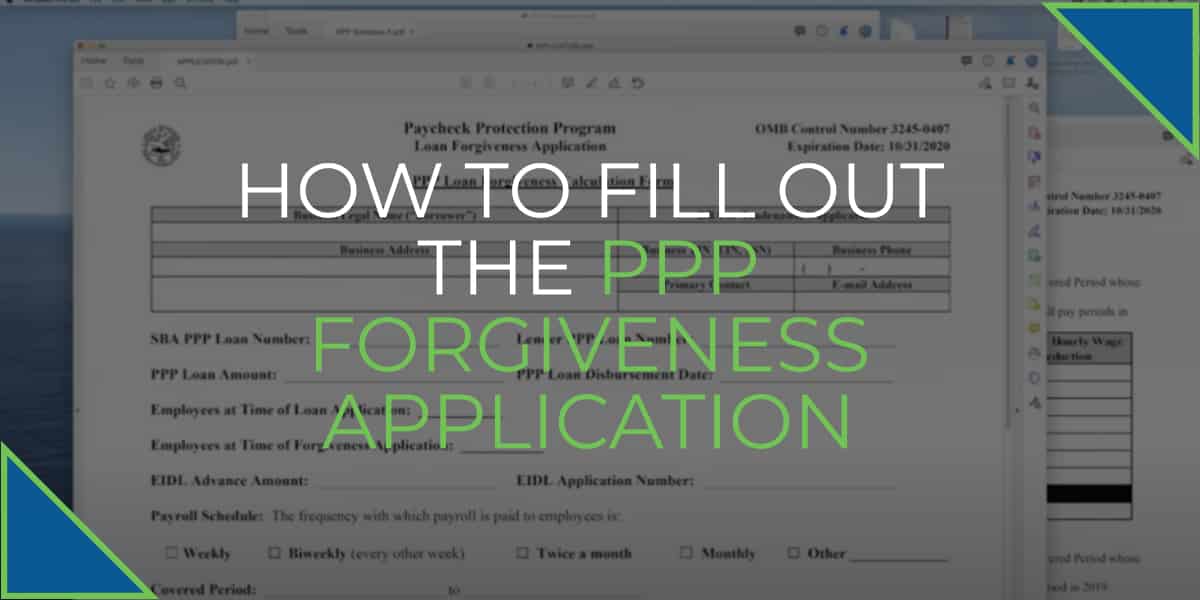

Step 1: Download the PPP Forgiveness Application

To get ready for this, the first thing you should do is download the application. You can just Google it. Just type in PPP loan forgiveness application. It’s an 11 page PDF that has the three sections. The application has three pieces that you should know about. There is the application itself, and I know you can see my screen. I’ve got them kind of all over.

There’s the Schedule A, and then the Schedule A worksheet. My recommendation is, the first thing you should do is you should work off the Schedule A Worksheet. Then do the Schedule A Form, and therefore complete the application.

Step 2: Gather Employee Information of Those You Paid During the 8-Week Period

There’s a few things that you’re gonna have to gather prior even being able to plug in the information. The main thing related to payroll would be all of your employees that worked during your PPP period. The last four digits of their social, their gross wages, and their average hours during that period. You will also need to have the employee’s average pay during… (There are three stated periods you can choose from to identify what their average pay.)

They’re going to ask that because they want to know if during the PPP period, basically the salary was reduced from what it was prior to the PPP timeframe. Any mortgage interests or loans basically related to mortgage or personal property, vehicles equipment, anything like that, those need to be in effect prior to February 15th on this application. Also lease payments, rent payments, and utilities. So utility is not just water, gas, and sewer. It also includes transportation. Which I interpret to be mileage, in addition to telephone and internet bills.

Step 3: Start With the Schedule A Worksheet

So, let’s start with the Schedule A Worksheet. The first thing it wants to do, and this is just giving you, if you have more employees and what would fit on this and this is for your calculation purposes. just open up a spreadsheet and create the same thing. Then add all of your employees on there, which will probably help calculate those totals. Basically Table 1 and Table 2 just allow you to enter your employee information, who they are what they got paid, if they’re full-time or not full-time equivalent, and basically if they have any reduction in hours. The first thing you need to know is for all employees that reside in the United States. You cannot include any owners on either of this calculation.

Step 4: Separate Your Employees into Those Who Make Less Than/More Than $100,000 and Full Time/Part Time

Table 1 is for anyone that has been paid less than $100,000 in 2019 or any employees that have not been paid in 2019. So anyone that’s new. In Table 2, it wants you to add the employees that were paid more than $100,000 in the 2019 period. Basically it separates in that hundred thousand dollar line between the two employee types. What you want to do is an employee name go ahead and put that in put the last four digits of their identify employee social security number.

Cash compensation includes gross wages, sick pay family, sick leave, any severance packages, and again the instructions, which is part of the original 11 pages, has this detail but again I’m just giving you a basic overview. The average full-time equivalent: iff you have an employee that works 40 hours a week that is considered an equivalent of 1. If that employee works 45 hours, you cannot go over 1 so 1 is the max. If you have any employee that works less than that, you can use a basic calculation that allows you to put a .5. So two .5’s equal 1.

The reason they’re asking for the full-time equivalent is they want to make sure that you started with the same amount of employee full-time equivalents that you ended with in the PPP period. Now there are going to be some cases where an employee was fired. They might have quit. You do have the option to have an exemption for that, but in this case they want you to go ahead, and and just put in that they are full time. If they work 35 hours a week you can take that 35/40, whatever that amount gives you round it to the nearest tenth, and you can also put that there. Or you can use a .5 if it’s under 40. The salary hourly wage reduction: I’m going to just explain this on, hopefully what sounds like a basic scale.

You cannot have reduced anyone’s wages more than 25% of their average wage at your reporting. If the average wage was a thousand dollars, and now they received seven hundred dollars per week, that’s actually more than 25 percent. Because 25 percent would have allowed them to make $750. Because there is a $50 difference from the 25 percent to what they actually got paid, that’s what you would put in this box right here, times the 8 weeks. It would be four hundred dollars. Again, if you are within 25 percent of a reduction in in wage, you do not have to put it here. This is anything over 25 percent. So, you’re going to fill all this out. You’re going to put your totals in here. Then we’re going to use that in the Schedule A Form. Down here, it’s asking for the numbers I had mentioned to gather. Your full-time equivalents, you can put your your numbers based on filling out these, step one through step five.

Step 5: Plug Your Number Totals into Schedule A

Once you’ve completed this, then you can basically plug in those numbers, the totals, into the Schedule A. If you look here, this goes box one, box two, box three, box four, box five. Line one through line five is all coming from the schedule A Worksheet. Now everything I’m telling, you remember it’s it’s a little bit more depth, but I’m just giving you a basic overview on completing the application.

Step 6: Enter In Any Health Coverage Information, Retirement, & Local Taxes

For line six, it’s asking for you to state your employee health insurance coverage or benefits paid by the employer. Do not include any employee paid contributions. You would go ahead and total that over the period. I should have mentioned this at the beginning, but there’s actually two periods that are accounted for in here. There’s the covered period, which is the first day of funding, basically the day you receive the money and it’s 56 days from there, or there is the alternative payroll covered period. If you ran a payroll that was after the day you got funded, you are allowed to use the first day of the pay period after you were funded as the first day of your 56 days. As long as everything falls on the right rotation, you would be able to include

that into your application for forgiveness. It does state that it wants you to in the application notify which period it is, and actually give you the dates for both. When you’re accounting for cost, they understand that it falls into the right period based on what it is. The alternative payroll would only be for, likely, payroll related costs.

A Note On Owner Income: Okay, so, I should have mentioned that at first, but it is here now. Right here, you have contributions to employee retirement plans. Again, this is employer portion, not employee portion. Then any state and local taxes, so unemployment would be that. If there’s any city or local tax related to employee wages, you could include that here because that would be paid strictly by the employer. In line nine, it does want you to include any amounts paid to partners or self-employed or general owners. The owner, still follows the same rule of the hundred thousand. Whether you’re an owner or you’re an employee you cannot make more than the $15,385. I believe it is which is at a hundred thousand dollar salary.

So if you were an owner, and you paid yourself fifty thousand in the eight-week period because for whatever reason you did, you would only be able to claim the 15,385 per owner because of the hundred thousand dollar rule. They came up with the hundred thousand dollar calculation for owners to say you take a hundred thousand divide that by 52 weeks times eight weeks equals that $15,385.

Line ten, you know just follow the calculation. Equivalency reduction calculation, if you have not made any reductions then you are not going to have to worry about any of this information.

Step 7: Gather Your Original PPP Loan Application Information

Okay, the last piece is the application itself. You need to have your PPP loan number, your disbursement date, your loan amount, how many employees you had at time of application, and so on. That’s pretty self-explanatory. Keep in mind that the frequency when I talked about the covered period or the alternative payroll covered period, you have to be on a biweekly or a weekly schedule to be able to use that period. Even if you’re twice a month, which I think that those people are not going to get that potentially good side of the stick, they do not unfortunately have the option to use the alternative payroll period.

The rest here as you can see, you’re going to go ahead and just enter your payroll costs, but you’re going to get it from your Schedule A. On your non-payroll costs: any interest on, again, personal or real estate property, any rent, or lease payments, and any utility, which also includes transportation, telephone, and internet. All of this has to be in place prior to February 15th, and you’re going to have to show documents that all of that was the case in your forgiveness application.

Then you’re going to, again, take the information that you got from Schedule A, enter that related to FTE’s, and it’s asking for a calculation to make sure that the payroll costs are in the seventy five percent split. Which again, this might change. That’s a basic overview of the application. There will be more to come. So we will go ahead, and get an updated video when that time

comes. Thanks for watching!

If you need assistance reviewing your current financials, contact us today! We’re here to help, and we offer a free financial analysis that you can use to your advantage!